Carbon Removal's best quarter yet

From July to October 2023, the business of CDR saw its biggest credit purchases yet, the biggest acquisition ever, and significant government funding from the US Dept. of Energy

You’re reading Terraform Now, my newsletter on the business of carbon removal. To support my work, you can subscribe here or share this article with interested folks

TLDR: Q3 2023, was the best quarter yet for the Carbon Dioxide Removal (CDR) industry. There were a few big milestones:

CDR providers signed big deals with the world’s most valuable tech companies

Two scaled DAC plants announced record-breaking plans thanks to >$1B backing of the US government

Carbon Engineering, a Direct Air Capture provider, was acquired by Oxy for $1.2B — by far the biggest CDR aquisition ever

It took us centuries to build an economy that warms the planet, and it is taking decades to build an economy that can solve the warming problem. Reading the climate discourse, I sense impatience with the business community. Critics want businesses to not just set nebulous targets, but spend their budget to counter emissions. Some argue that companies will never do this, and government should step in and make major changes to the 200-year old capitalism contract. The least governments can do, goes this line of thinking, is institute a tax on emissions.

Three recent developments in Carbon Dioxide Removal (CDR) should give pessimists cause for hope. From July to October 2023, Microsoft, Amazon, and Apple signed the biggest deals yet to purchase CDR credits. The biggest companies in the world are now paying to take CO2 out of the sky. At the same time, the American government released over a billion dollars in funding to build new CDR plants on the Gulf Coast. Finally, an oil behemoth bought Carbon Engineering, a leading CDR technology developer for $1.2B.

All of this happened in America & Canada, neither of which have a carbon text. This suggests that, at least when it comes to CDR, capitalism may not need a redesign to make progress on climate.

Big Deals from Big Tech

In early September, Microsoft announced that it would purchase 315,000 CDR credits. This means that Microsoft will pay Heirloom Carbon a few hundred dollars each time Heirloom removes a ton of carbon dioxide (CO2) from the atmosphere. Microsoft will certify that those tons are dedicated to Microsoft, meaning they can’t be sold again to other buyers. Double-dipping would be considered fraudulent, even if it doesn’t break any actual laws.

Fraud is a serious problem in the carbon credit industry, as Heidi Brooke laid out in a recent New Yorker piece:

Yet it is extraordinarily difficult to quantify how much carbon these schemes really save. To do so, you must demonstrate that the forest would have been razed without protection—a counterfactual that is nearly impossible to prove. There are also issues of “leakage”: even if the agents of deforestation are driven out of one area, they may cut down trees someplace else. Then there is the question of permanence. Greenhouse gases can linger in the atmosphere for thousands of years—but forests are vulnerable to wildfires and other calamities, and most protection schemes last no more than a few decades

In this piece Brooke is mostly discussing reforestation projects, where a carbon credit provider offers to plant X trees for Y dollars.

High-quality CDR, like Heirloom’s Direct Air Capture (DAC) technology, is different. These are industrial processes that can be measured using sensors. Microsoft can visit the site as much as they want — they could even plant someone at the Cypress Plant in Louisiana where CO2 removal will happen. And because Heirloom’s captured CO2 will generally be stored underground, it is permanent in a way that planting trees can never be.

In the 2010s, businesses looked for a quick fix for their emissions and bought cheap, reforestation credits. They did this in part because it was the only gig in town, but also because the credits were $10 per ton of CO2, buyers could get a lot of bang for their buck.

That is, until many of these projects were revealed to be frauds. Now buyers are much more mature. Instead of going for many, cheap credits, they are choosing fewer, more expensive, and higher quality credits. Three indicators of quality — permanence, verification and transparency — now top the list for CDR buyers:

Back to Microsoft. Just after they inked a deal with Heirloom, I predicted that Amazon, a close competitor in the all important cloud market, would be forced to follow, working with either Climeworks or Occidental Petroleum (Oxy). Sure enough, Amazon then signed a >$150M deal with 1PointFive, Oxy’s sales and marketing arm.

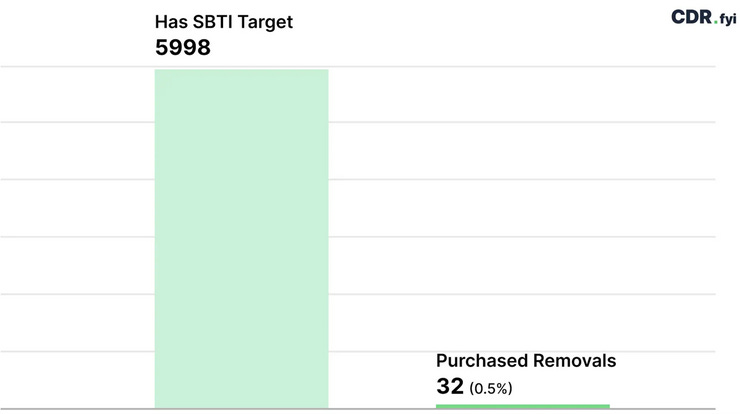

And this is just the beginning. We can sort out what organizations are potential CDR buyers by focusing on companies with an SBTi1, which is a fancy way of saying that these companies have prioritized reducing their emissions. According to cdr.fyi, only 0.5% of these companies have purchased credits:

Don’t get me wrong, CDR will have challenges convincing customers that it’s worth spending their small climate budgets on pricey credits. But some companies will look at Microsoft, Amazon, and early buyers and conclude that CDR credits are a good way to diversify and offset emissions that they don’t have a path to mitigating.

The key issue for many of these buyers will be supply of credits. That 315,000 ton deal that Microsoft and Heirloom signed represents ~100x more credits than Heirloom has every produced. And Heirloom is not alone — every CDR project today is tiny.

Enter Uncle Sam

The American Department of Energy is looking to change that. In August, it announced that it would give $1.2B to two groups that will build large Direct Air Capture (DAC)2 plants on the Gulf Coast.

These projects are exciting for a lot of reasons:

Scale: Each plant will capture (up to) 1M tons of carbon dioxide per year. That’s >100x the scale of the largest DAC plants operating today

Geography: Texas and Louisiana are right next to each other, and both projects are close to the coast of the Gulf of Mexico

Geologic storage potential: A recent study of the Gulf Coast Miocene, a thin layer of geology along the coast, found 125 billion tons of potential CO2 storage — that’s enough storage for three years of global emissions at 2023 levels.

Skills: The gulf coast region is full of chemical engineers and geologists looking to move on from the oil and gas industries

I have much more to say about this DOE program, both good and bad, and wrote a long post on it when the news broke:

I hope that in the medium-term, there is enough demand for CDR credits that extra government funding won’t be necessary. But in the short-term, this program will play a big role in not just getting the plants built, but also making CDR legitimate in the eyes of the broader market. The scientists at the DOE think CDR has legs, which will give even more buyers confidence that carbon removal is here to stay.

Carbon Engineering’s $1.2B exit

Just a few days after the DOE announced $1.2B in funding, Occidental Petroleum (Oxy), made a $1.2B announcement of its own, an agreement to purchase DAC technology provider Carbon Engineering. At the time, I wrote about the many reasons this deal makes sense, and sounded notes of caution. Here I’d like to focus on the longer-term impacts for CDR.

(1/3) Learning from failure: A lot of people are rooting for Oxy to fail because it is an oil company — the big bad for most environmentalists.

Failure is valuable because it teaches the industry what not to do. I’m personally bullish on Oxy’s ability to capture CO2 because they have so much experience building petrochemical plants, which are similar to Carbon Engineering’s liquid-based tech. But even if Oxy is able to make big DAC plants, they can still mess up. As I wrote at the time of the aquisition:

My guess is that Oxy will do very little true geologic storage, instead engaging in Enhanced Oil Recovery (EOR) and making recycled fuels. EOR pumps CO2 into active oil wells, increasing the pressure and pushing out more hydrocarbons. Recycled fuels — also called synthetic or drop-in fuels — use captured CO2 to make gasoline for cars, trucks, etc. EOR is a core part of Oxy’s drilling process, while marketing fuels of all kinds is a core part of Oxy’s go-to-market. Oxy might relish the opportunity to market fuels made with DAC.

Let’s say that Oxy uses 90% of it’s captured CO2 to do EOR. It then sells credits to Amazon. In 2027, Heidi Brooke writes an expose showing how terrible it is that Amazon’s climate budget went to pumping more oil out of the ground. Amazon cancels its contract with Oxy, and other customers follow.

That would all be very bad for Oxy, but good for the companies that are focusing on permanently storing CO2 underground or in cement without creating new emissions. Customers will again flock to high quality, transparent credits from Climeworks, Heirloom, and others.

This may not be Oxy’s path to failure. The point is that there are dozens of ways Oxy can fail, an each of them holds a lesson for the CDR industry.

(2/3) Oxy might succeed: Yes, an oil company might make the green trasition. Stranger things have happened. And there are a lot of reasons Oxy & Carbon Engineering are good for each other:

Technology: Carbon Engineering’s liquid-based tech is a nice fit with Oxy’s chemical engineering expertise

Full stack: Oxy has arguably the best sales & marketing engine in the industry in 1PointFive, and has already inked big customers

Revealed ambition: It seems unlikely that the Carbon Engineering board agreed to the aquisition just for the money. Oxy must have shown a good strategy and a genuine desire to win the DAC market

Here’s what I’m monitoring from Oxy going forward:

Credit delivery: 1PointFive has made massive DAC sales, but can it deliver? Will they actually build 1 million ton capacity at both plants?

Impact on carbon removal: What is the split of permanent storage, EOR, recycled fuels, and other uses for capture CO2?

Cost of DAC and slope of the learning curve: What is all-in $ per ton of CO2 captured at Oxy’s plants?

Revenue: What is Oxy’s avg. revenue from a ton of CO2?

Shareholder value from DAC: In 2033, how much of Oxy’s market cap will come from fossil fuels vs. carbon removal?

Success is not just about Oxy’s stock price. It’s about building a sustainable business removing CO2 from the sky while providing value to shareholders, customers, and employees. Oxy’s DAC business might fail even as it drastically brings down the costs of Carbon Engineering’s liquid-based DAC (#3 above), then spins it off. That’s why we have to monitor all of these metrics independently.

(3/3) Capitalism & Climate Tech: Many of the folks who get into Climate Tech have a rebellious, idealist personality:

I think profits are actually good. Entrepreneurs should be rewarded for solving tough problems, otherwise no one will try. Take David Keith, a 60-year-old professor who started working on CDR in the 1990s before co-founding Carbon Engineering in 2009. In the popular imagination climate tech entrepreneurs are 27-year-old Stanford graduates looking for a quick buck. But in capital intensive industries like CDR, patient, farsighted founding teams will win, and should get a payday3.

Of course most profits don’t flow to founders and investors. Executives mostly reinvest profits in improve the company by hiring new people or improving the product. A company turning a profit usually has product-market fit, which draws in more investment, which helps the company scale and extend its product-market fit to more customers.

This is exactly what happened with Carbon Engineering, which built a compelling product that Oxy and Chevron both wanted to use in their DAC plants. The fact that multiple customers vetted the technology gave Oxy the confidence to buy Carbon Engineering and commit to scaling it up4. That, in turn, gave Amazon the confidence to buy credits from the new combined entity. That will increase demand for Oxy’s credits, assuming what they deliver is high-quality, permanent, and transparent. All of that seems pretty good to me!

This big exit is going to attract more talented entrepreneurs into Climate Tech, not repel them.

Momentum

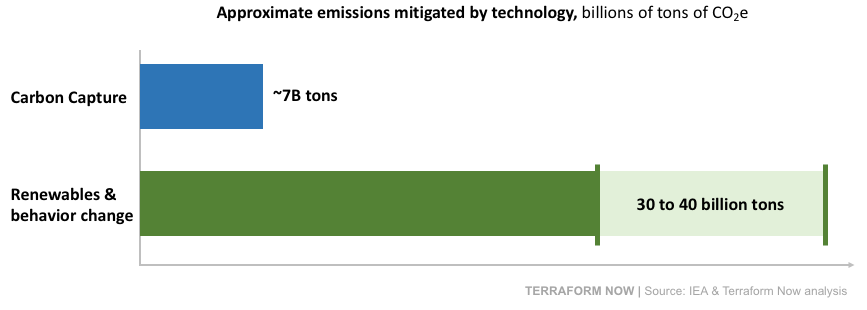

CDR has a long way to go. The DAC plants that broke ground this year might be able to take out ~2M tons of CO2 per year, about 0.03% of the IEA’s target of ~7B tons per year, sometime in 2026. I believe we will need way more than 7B tons per year of CDR capacity because it’s unlikely that we reduce emissions below 15-20B tons of CO25 per year.

But these plants represent real progress. Each are >20x larger than any existing DAC plant.

In the same vein, it would be great to see more government funding for CDR, especially in Europe and China. But the fact that the United States went from having a backwards climate policy to funding cutting edge climate tech is cause for celebration.

And as I’ve argued, even the big paydays for Carbon Engineering stakeholders. Who knows, maybe Oxy will become a big green champion.

SBTi = Science Based Target, which “provide(s) a clearly-defined pathway for companies and financial institutions to reduce greenhouse gas (GHG) emissions, helping prevent the worst impacts of climate change and future-proof business growth.” click here for more

Direct Air Capture is one form of CDR, and tends to get the most attention from VCs and customers. I have written about of DAC technologies here

I would even suggest the investors who stuck with Carbon Engineering for over a decade deserve a payday! Crazy, I know

The DOE funding also helped Oxy see that DAC, and particularly Carbon Engineering’s vision for liquid-based DAC, had real advantages

The emissions construct we care about here is actually CO2e, meaning greenhouse gases equivalent to the same amount of CO2

Great insights and the description of Occidental’s approach.

Is there any significant DAC happening in areas like Saudi Arabia or the North Atlantic or Indonesia, for example?